Revisiting my 2013 call to Stop Bail-ins and Break up Too-Big-To-Fails

In September 2013, while still a volunteer with the Canadian branch of the LaRouche Movement, I found myself spearheading a campaign to break up the banks of Canada and shed light on the incoming Bail-in legislation being set up to loot depositors’ accounts. One of the associated fact sheets which I authored outlining the dysfunctional Canadian banking system and the necessity of breaking up the bankrupt ‘Big six’ banks is sadly still as relevant as it was 10 years ago.

As part of that campaign, my former colleague Jean-Philippe and I decided to produce a series of educational videos to present the topic of bail-ins, national banking and other systemic reforms to a Canadian audience.

Due to the renewed push to invoke those bail in regimes across Canada as outlined by the brilliant Ellen Brown this week, I though it worth while to republish the full transcript and video recording of our September 2013 CRC Leadership Discussion (Cyprus Bail Ins Come to Canada- Stop Bail ins Now), alongside the accompanying issue of Canadian Patriot #6 which you can download here.

Cyprus Bail-ins Come to Canada: Pass Glass-Steagall Now (Transcript)

Welcome to another edition of the CP discussion My name is Jean Philippe Lebleu, and I’m accompanied here with Matthew Ehret-Kump, Editor of the Canadian Patriot. Today we are going to talk to you about the actual financial world economic crisis, focusing most specifically on the latest developments surrounding the nation of Cyprus, and the implications of what is happening there for the whole world and most specifically for Canada.

For a start, just to clarify a few things for people regarding this crisis: What we are seeing unfold, especially since 2007-2008, is actually the result of a decades long crisis that really started in the 1970s where there was a radical shift away from our system of national development, away from the productive powers of labour towards a money policy, where money became the basis of the world’s economy. So we went away from science. We went away from industry, education and healthcare, and towards this idea that money is the master.

People are most familiar with what has happened since 2008 when various major banks effectively went bankrupt which then led to a policy of “bail outs”. Those policies started with the end of the Bush Jr. administration which was continued very fervently by the Obama administration as well as in Europe by the European Central Bank. This was a policy that saw governments buying out the toxic assets of those various banks (JP Morgan Chase, Citigroup, etc), in order to keep those banks afloat. But obviously that meant that various governments had to implement policies of massive austerity on their population. Now we’ve all heard various horror stories from nations such as Greece or the United States where people need food stamps to survive, old people cannot aford their medication, unemployment and the increase of the suicide rate in Europe, etc.

So there are physical consequences of these bailouts accompanied with another aspect of this policy which has been called “Quantitative Easing” (QE), which is basically hyperinflation. In QE, various institutions were involved in printing a lot of money to try to keep that banking system afloat.

Now one of our colleagues, Dennis Small, in the United States made a small graphic of that Quantitative Easing that features the $4.4 trillion dollars printed over 4 years as a form of hyperinflation.

As you can see on this graph, the actual banking activity has been substantially reduced, meaning money has not been leant to the real economy as it should have been. The other little red line that you see at the top represents what wee call “Quantitative Stealing” which is the new form of insanity which we see in the ongoing attempt to sustain the imperial banking system called “bail-in” [Graph 1]. Now we’re going to jump into that question, and try to come to understand what that exactly is. So I’d like to start off to let Matt explain what’s the situation in Cyprus, and how this affects the world situation and Canada in particular.

Matthew: Okay. I think you’ve laid it out pretty well. What we’ve been experiencing over the past four years is a complete breakdown of the system. Its not a recession as the media has promoted it, as something which just comes around organically every few years and has ups and downs, bulls and bears. What’s happened is that we’ve come to the end of a process that was really kick started in a serious way with what you mentioned, as the period in the early 1970s when money and all values were disassociated not just with gold, but rather the entire productive process underlying nation states. So to have a sovereign nation state, you have to be producing real goods, thinking long term about your infrastructure and your science, in order to overcome your limits. Not just consuming in a post industrial model. And that was the way that people used to do things. Call it what you will, and there were problems with it, but the principle was “money was not the source of value”, it was “what are you doing for the future”?

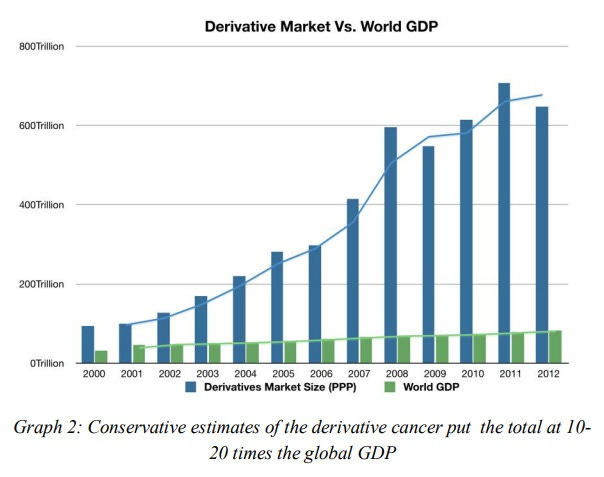

Now when this was destroyed with the Bretton Woods System, we fell into an insane logic of reproducing a monetary system which operates as a cancer, by finding new ways of gambling, new ways of putting values on price differentials, securitizing assets then betting on the insurance on them which has far outpaced the actual securities underlying the nominal “money” so called which is being bailed out. This is of course a reference to the problem of derivatives. So you can’t print more money to bail these out anymore. They are upwards of twenty times the global GDP. Best estimates place these anywhere from $600 trillion to $1.5 quadrillion dollars, which is 10-20 times the entire world’s GDP [Graph 2].

Where we’re at right now is a new phase of the collapse, where what has happened recently in Cyprus is now the template for the world. What the British Empire is saying is that rather than go in from the outside using central banks injecting tax payer liquidity to buy up toxic assets to put on its books as the Federal Reserve and European Central Bank have been doing, or now the Bank of Japan, rather than do that, what they’re saying is “now we’re going to have a “bail-in”. We’re going to take uninsured deposits, savings, RRSPs, anything outside of the $100 thousand euro government insured limit, we are going to essentially steal that, and put it directly into the failing bank that needs the funds, or else its going to collapse.

So right after this was done in Cyprus, shock waves were felt throughout the world, echoing the danger of bank runs… the same type of thing we had in the Great Depression. This is where people are saying “if I can’t keep my money safe in the bank, I have to take it out”, and this is what’s in danger of setting of the destruction of the system.

As soon as this event happened in Cyprus, Joern Dissjlebloom who is Holland’s Finance Minister and head of the Eurogroup said that this would be the template for all of Europe. The next day, Hans Knott who is on the Board of Directors of the Bank of International Settlements (BIS) said that this approach “will be part of the European liquidation policy’, meaning this is for the whole eurozone.

What this was for those who are not completely familiar, 37% of all deposits over the $100 thousand insured limit are being converted into “common stocks” in the Bank of Lykie and the Bank of Cyprus, which are the two banks which needed the injections. 22% will never see interest , and the remaining 40% you will only get back if the banks get healthy again. So right now everyone rushed to the banks, to the ATMs only to find out that they were closed. They were locked down for a week. And when the banks finally opened again, you couldn’t get more than 300$ out of the bank in a day. So this is shutting down businesses, and wrecking havoc just like we are seeing in Greece, Spain etc. and also increasingly in the North American continent too where you have had a total destruction of your physical economy.

And so now people like Dijsselbloem and Hans Knott said, “Oh no! We meant to say that it wasn’t a model for all of Europe. We only meant to say that it was only for Cyprus. We didn’t really know what we were talking about. It won’t spread. We won’t really take people’s deposits.” But what they really want us to forget is what the Troika which is the ECB, EC, IMF originally told Cyprus to do in the very beginning of this whole debacle… which was to take even the insured deposits, i.e. to take the 6% insured deposits and 10% above it. This policy was rejected by the Cyprus parliament. So it shows that they are willing to go to any lengths to keep the system from melting down even if it means depriving people from their own basic means of existence.

Now I brought up the Bank of International Settlements (BIS) because what we have discovered over the past week is that this approach of bail-ins was not cooked up overnight. This has actually been planned for a long time. What we are seeing now is the uncovering of the official policy documents sponsored by the BIS, BoE, Federal Reserve, to co-ordinate a global bail in strategy.

They only poked Cyprus to see what they could do. But now that they have a certain feel for it, they want to officially institutionalize it globally. And on Dec 10th, 2012, there was a policy paper of Bank of England, now run by Canada’s Mark Carney and the Federal Deposit Insurance Corporation (FDIC), called ‘Resolving globally active and systemically important financial institutions’ . This paper directly called for measures which would allow for the conversion of deposits into shares just to keep the banks alive. But there is a whole slew of documents even before this one was published callings for the same policy all coordinated by the membership of the BIS’s Board of Directors.

Now for people who think that the Canadian banking system is some sort of a model for the world system because we are so conservative in our banking culture, we’ve got news for you… our Canadian Action Plan of March 22th 2013, referenced the BIS (which has a branch called Financial Stability Board (FSB)) which is also run by Mark Carney, which said that it has been following the BIS policies since 2011. The following is a small quote from the Canadian Action Plan which demonstrates that:

Canadian Action Plan, March 21, 2013, p.145:

“The Government proposes to implement a ?bail-in regime for systemically important banks. This regime will be designed to ensure that, in the unlikely event that a systemically important bank depletes its capital, the bank can be recapitalized and returned to viability through the very rapid conversion of certain bank liabilities into regulatory capital.”

The Nature of the Beast

Now what exactly is Mark Carney? This understanding will give you an idea of the British Empire monetary machine which generates global policy. To put it simply, Mark Carney is a Goldman Sachs guy, he isn’t Canadian… He’s Goldman Sachs! That’s what his job was before being brought into the Governorship of Bank of Canada. Mario Draghi, the guy who preceded Carney heading the FSB, was a Goldman Sachs guy who then was brought into the central bank of Italy and has been a major opponent of our movement for years.

Now, Mark Carney’s and Mario Draghi’s job is to make sure that the will of the Empire is maintained. And the will of the Empire is international. It is not a nation ruling the world, it is not a mystical thing. The power of finance for an oligarchy which has long been known as the British Empire has never disappeared. If anything, it is more powerful today in one sense but ironically in another sense, it is also much more weak because their financial system is collapsing.

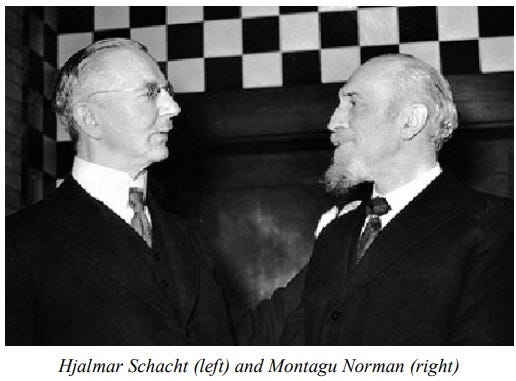

So the BIS for which Mark Carney works, is a very useful thing to look at, because it gives us a sense of the pedigree. And I’ll go through something because I was watching a documentary the other day called ‘Banking with Hitler’ (1).

This is something that was done in 1990’s by the History Channel, and what it goes through is how the BIS was created by none other than the Nazis. It was created in 1930 by Hjalmar Schacht , the Nazi Finance Minister and the Head of Reichsbank with the guidance of Montague Norman, the head of the Bank of England who was also a major sponsor of the Nazis.

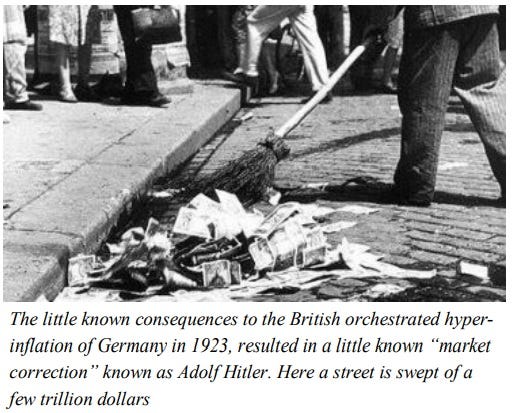

The BIS was created for a very specific reason. First of all , in 1920’s, you had hyperinflation in Germany induced by the BoE, the Federal Reserve and other allied powers which told Germany to print infinite money, do whatever it takes to just pay its debts, even if it meant sacrificing their currency, which Germany did. You have those famous pictures today of people back then taking wheelbarrows of money to buy bread.

So this crisis created a shock effect in the population where even after having trillions of dollars but no bread to eat, the population was psychologically induced by Hjalmar Schacht, the BoE and others to trade in all of their trillions of dollars of printed Reichsmarks for new Rentenmarks.

With this came new laws of massive austerity, lowering of living standards, fascism…. Because a democracy would never accept those cuts of living standards. So this massive change in economics and exchanging of trillions of Reichsmarks for the new Rentenmarks could not have been done by a regular banking system. They needed to create a central bank for the central bankers. This was the BIS.

After the war got under way and every single nation that Germany had taken over starting with Poland, Czechoslovakia, Holland, France, Belgium, the Germans would not have been able to keep building their war machine if they hadn’t taken those nations’ gold and finances, which were then kept where? In the BIS! So the role of people like Montague Norman, the BoE and those who occupied the Board of Directors was to ensure that there was a smooth transition of gold which was taken from these occupied nations into the German war machine. And this goes on until the war is far underway and people are dying in the mud.

So what was the intention? To create a global fascist regime. Why else were Wall Street, the Bush family, the Queen of England’s uncle, why were they part of a global banking apparatus funding fascism as the solution to the economic woes of the 1920’s?

Well, they wanted a global dictatorship enforced by these psychopathic, egotistical narcissists like Mussolini and Hitler. This is why they chose Barack Obama. They want these kinds of systems and they want these kinds of narcissistic dictators because that’s the most controlled system an oligarchy can rule over. And fundamentally, this is what never disappeared even after the Nuremburg. This is the system which had increasingly taken over our society since the death of John F. Kennedy and since the destruction of the Bretton Woods System in 1971.

And now we have come to a point where either we go towards what Franklin Roosevelt was doing which starts with Glass-Steagall, not fascism which was being implemented at the same time in Europe. And Glass-Steagall is the thing which people like Mario Draghi, Mark Carney and Ben Bernanke have been assigned to stop at all costs. Because this now is in Europe as a policy. It is in the USA.

Jp: Yes I think we can say that similar to today what going on in Cyprus where a bank holiday was declared, you had a similar crisis under Franklin Roosevelt who had also declared an emergency bank holiday. But what came out of that was actually a very efficient cleaning up of the system. So everything with no intrinsic value was just written off the books of the banks. And the legitimate banks were reopened after the 11 day bank holiday and activities could continue but they were under the guidance of the Glass-Steagall law. The commercial banking was separated from the investment, speculative banking. So the speculators could gamble with their own money and eat each other but the commercial economy was untouched and protected. Now as you said, Canada’s also adopting a bail in policy. And a lot of Canadians have been led to believe that our banking system here is somewhat different ; that we have a different banking culture. As if that makes us somehow nice people where we don’t see risks. But this is a lie. And I know Matt, you wrote an article on the present Canadian housing bubble (2). Also, we discussed the famous bailout that occurred in Canada in 2010. So could you say a few words illustrate the situation here as to why we are in the same dynamic as the rest of the world?

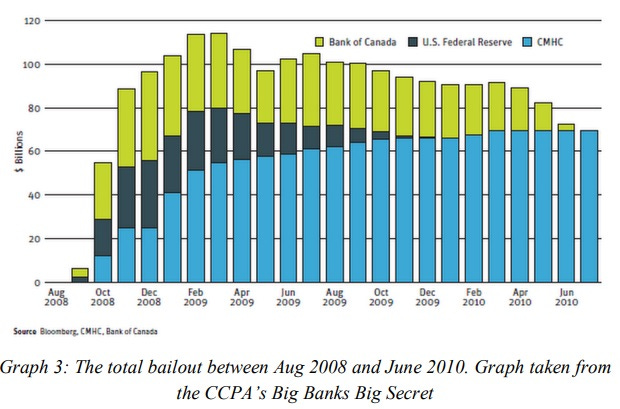

Matt : Yes, this came to our attention in a new form in 2012 with the Canadian Centre for Policy Alternatives (CCPA) who wrote a very important report “Big Banks Big Secret” (3) that just illustrated that what everyone believes about the soundness and stability of the Canadian banking system is founded on a deep-seated fraud. That, if it were not for the $114 billion bailouts between 2009 and 2010 injected in the Canadian banking system, it is probable that at least three of the big 6 banks could have collapsed [Graph 3].

This was not just some emergency liquidation injection to the banking system as Mark Carney said. This was a bailout. So the bailouts given to CIBC, BMO, Scotia bank for the 2009-2010 interval actually exceeded the market value of those banks.

So how did this work out? This wasn’t a typical bailout , like what you saw in Europe and USA. It was a little different than that. What happened was that three conduits were used. As the CCPA report shows that you had the Canadian housing and mortgage corporation (CMHC) which provided most of the bailout. They produced $67 billion to buy toxic Mortgage Backed Securities and other things from the books of these banks. The Bank of Canada and the Federal Reserve were the other 2 institutions that provided emergency liquidity for the banks. The CMHC had to create something called the Insured Mortgage Purchase Program, specifically for this injection. This was done primarily because Canadian economy is driven by financial gains. We don’t have a physical economy any more. We don’t have industry, we don’t manufacturing. Even though people think we are a “resource export economy” (i.e. we sell natural gas, agricultural produce and that makes up our economy), the fact is that these make up only 7% of our GDP. The housing sector makes up 27% of our GDP! So the latter is our economy at this point.

Now this type of service economy was created by the takedown of the Canadian Glass-Steagall (i.e. our Four Pillars). A lot of people, even policy makers who we talk to are not familiar with that we had such a thing called the Four Pillars for a very long time in Canada’s history which was taken down long before the U.S. Glass-Steagall was eliminated. The Four Pillars isn’t exactly the same as the U.S. Glass-Steagall but the principle was simply that financial institutions like insurances and deposits and securities and trusts are kept separate from each other. So you can’t have ‘too big to fail’ universal banking institutions like we have today.

Now how was this bubble created? Canada is sitting on top of an overgrown bubble as you have mentioned earlier. The big 6 banks were downgraded this year. Why were they downgrade? Well, partly because we have a huge amount of consumer debt which is out of control. This is something like 160% of people’s earnings vs. 110% in USA. Then you have the housing bubble which has exceeded the average price across Canada than the house prices in USA at the peak of their bubble in 2007 [Graph 4].

So when you look at a lot of regions like Vancouver, Toronto etc, the house prices over the past 7 years have doubled, in some cases tripled and quadrupled. And how is this being created? Well, by extending insurance of the CMHC into the securities sector which now securitized these housing loans, they were able to guarantee a super low interest to foreign investors at one side. So the people who had savings in hedge funds who were trying to save their money from the economic collapse are now putting their money anywhere which is considered low risk. So they put it in Canadian housing, considering it as a safe bet, as it’s going to be guaranteed if the house goes under.

So you have a lot these big communities where no one is living in these big houses but the house values are just going up because people are just buying up Canadian real estate while living in Abu Dhabi. So these are becoming more and more expensive so that people that want to have a family, want to live in a house, now can’t. Because they can’t afford one. On the other hand you have the diminishing interest rates being given to people who can’t really afford to buy a house so that they can get a mortgage at super low interest. So they can get in debt. A study was just produced which indicates that even if the interest rates were increased by 1-1.5%, you could have immediately across the board defaults of anywhere between 10-16% of our houses. Nobody could pay those mortgages. Let alone all of the overage built on top of whatever is securitized in that sector.

So now you have something which otherwise couldn’t have been created if the Four Pillars hadn’t been destroyed. The very act of CMHC which itself today is upwards a $600 billion of government, taxpayer insurance was only $50 billion at the time of the takedown of the Four Pillars in 1990’s by Mulroney to make way for NAFTA. And since Harper has come in, the ceiling has been successfully raised several times to 200, 250, 500 billion dollars to now to 600 billion dollars just to keep the bubble going because if that was not there, you couldn’t guarantee the investments, you couldn’t encourage the foreign investments, the hedge funds and other things to create these huge record breaking profits for our big 6 banks in 2011 [Graph 5].

And that is the additional irony. While everybody else in the world was tanking, our Canadian banks were coming out with huge profits and the key point that the CCPA draws out in their document is that the reason this hasn’t gotten more coverage is because Canada has the most opaque, least transparent banking system in the world. And this is big for a lot of people to really think about.

The only reason we are getting away with the lie longer than Europe or USA is because banks there have to demonstrate their risky exposures to derivatives on their balance sheets, whereas in Canada they are kept off those sheets because they will “distress investors”. Even the Bank of Canada won’t even tell you where pension plan investments and other funds in its coffers are invested in. If you were investing in JP Morgan, you would know immediately that JP Morgan has up to 78 trillion dollars of derivative holdings.

We know that easily. We know the quantity of the bailout in USA. This is all relatively transparent. In Canada, this is not. So we here have to go through much more digging to uncover this and most people aren’t equipped to do that.

So everyone is going to lose everything. I mean, this idea of a bail-in not being used in Canada because our banks are so sound, it’s bullshit! And Carney even pointed out in 2010 in a speech he gave to Geneva that he intended to carry this policy forward (4). Not because it’s his personal intention but because he is a Goldman Sachs man. He is used to following orders. And in this speech, he simply says first, that if bail-ins had existed at the time of Lehman Bros’ collapsing in 2008, instead of losing $150 billion, we could have just lost $27 billion. And then he goes on to say: “Statutory bail-in authority could fill a crucial gap in the resolution toolkit and should catalyze private alternatives to the restructuring process.” So you see what he is doing, right?

Jp : Yes, they are opening new doors to grabbing money. They make it vague but with the case if Cyprus, we see that it doesn’t seem there is any limit a government will put unless the government is a courageous one. Otherwise the bankers are just going to grab whatever they want.

Matt : and they are always pretending that somehow the system is fine and we can’t use government based solutions like Glass-Steagall. It has to be private based solutions. Carney goes on in his Geneva speech from 2010 that “an example of a promising market-based mechanism is to embed contingent capital and bail-in features into unsecured market debt and preferred shares issued by financial institutions…”

‘Preferred shares’, what is that? Well, that is exactly what happened to Bankia in Spain! Where over a million depositors were induced to put their shares into these Spanish banks to get ‘preferred shares’ simply meaning that you are going to get more interest than your common, usual shares. And as soon as they did that, the banks coordinately cut the value of all the ‘preferred shares’ which were 2$ a share down to 1€ cent. So they downgraded those preferred shares to common shares and the latter were given a ‘haircut’. It was more like a decapitation from 2$ to 1€ cent in 2 weeks which is the biggest theft we have seen so far. But again, these are small little guinea pigs being setup for the global solution which Mark Carney is pushing for. And he goes on in his same speech saying that “Its presence would also discipline management, since common shareholders would be incented to act prudently to avoid having their stakes diluted by conversion.”

So the axioms are just transparently disgusting. But statements like this betray the belief they want us to adopt which is that the behaviour of the bank is going to be made better if you had the bail-in regime. As if all the shareholders will now want the bank’s behaviour to be more “safe, sound and responsible” as if what determined the banks behaviour was the judgement of the shareholders. At no point in history has that ever been true. Nowhere did any shareholder vote to take down Glass-Steagall. The shareholders of the banks never did that for the Four Pillars in Canada. What you have is the BIS, the London banking networks run through Carney, through Rothschild banking cartels and these are the guys that issue and standardize global banking behaviour. Not the shareholder of the banks.

Jp : Yes, I think this is an important point to make that we are inside a very long, old fight between nation states and an Imperial system that has been using its control of banking to reduce nations to the level of simple colonies. Right now, we are going back to an old form of Imperialism which doesn’t mean a bunch of guys trying to make a lot of money. We are talking about policies of population reduction, seen in situations like Greece where unemployment levels are high, life saving medications are impossible to get etc. So you are talking about policies that kill people. So these people in finance will say “ let’s make those sacrifices to have ‘sustainable banking’. Well, at a certain point you have to decide what is your priority. Are you going to be totally blinded by a monetary policy in which the money is the cult leader or you are going to go back to nation building? How are we going to actually re-launch a real world economic recovery which means to sustain seven billion people or more? It doesn’t mean population reduction through green fascist policies of anti industrial development or massive austerity which is the policy coming from the British Monarchy (i.e. the Queen and her poodle Prince Philip). The latter has stated his population reduction policy many times (5).

Our banking system is falling down and all politicians from all parties have been playing the same audio cassette that “Canada’s banking system is the best in the world” which is a lie. So we have to tell them what’s really happening. At the same time, we have to get those people to realize that elections in 2014 are very far. There is a need for a mobilization to implement Glass-Steagall now; not in a year and a half. So we need to build some courage and get those people to drop their fantasy of winning the election. Something has to happen now, otherwise Canada’s economy is going to go down the drain.

So I would urge people who are watching to join our fight, go on out website to download the appeal for a Global Glass-Steagall which everyone should sign including your Member of Parliament. We also have on our website our mobilization leaflet covering what’s been discussed here so far regarding Cyprus, so get active with us, make a financial contribution and be part of our activities. I think that right now is the time to move. There is absolutely no reason to wait any longer. So thank you for watching and we will hear from you soon.